Copyright © 2025 Shenyang Dasan Pharmaceutical Technology Co., Ltd.

Posting Date:2023-01-13

Posting Date:2023-01-13 Views:

Views: Recently, the eighth round of national centralized drug procurement has been officially put on the agenda.

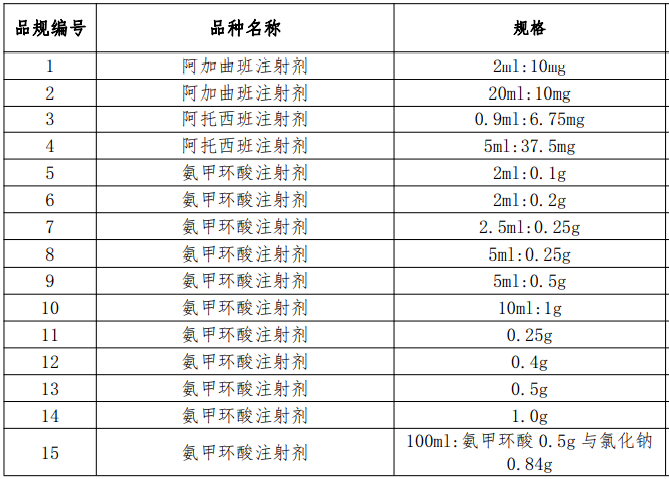

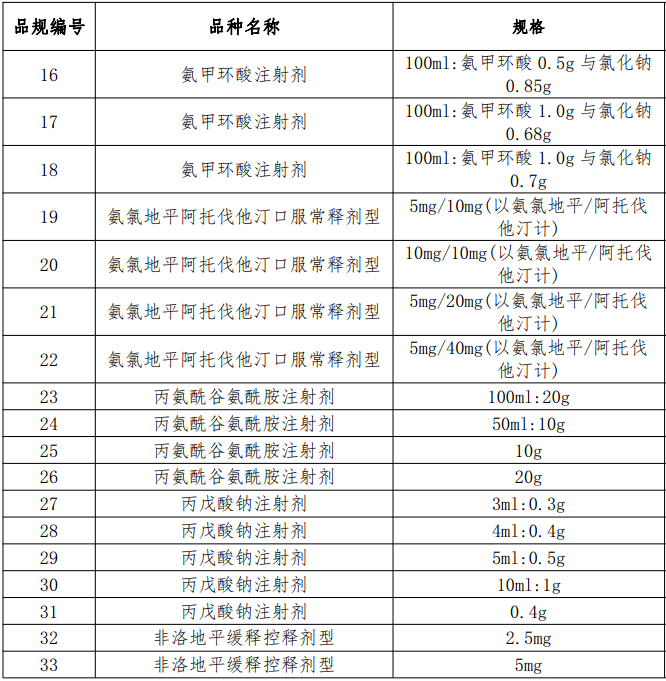

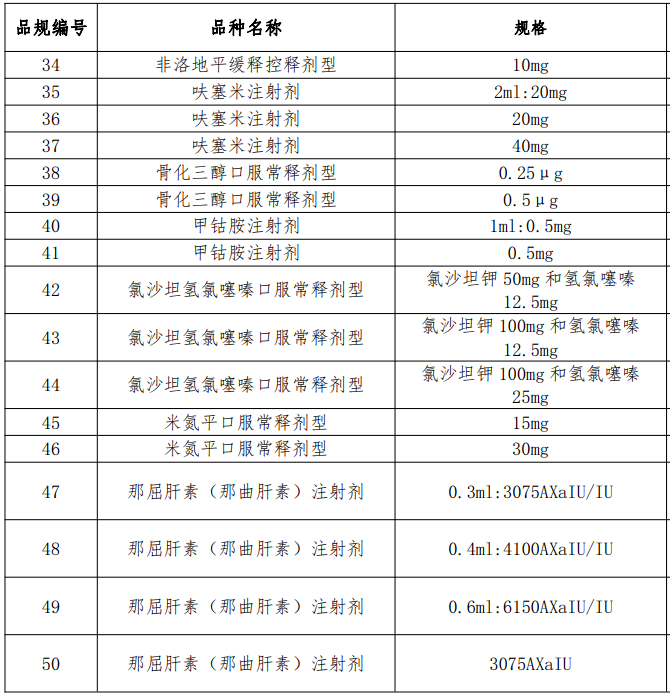

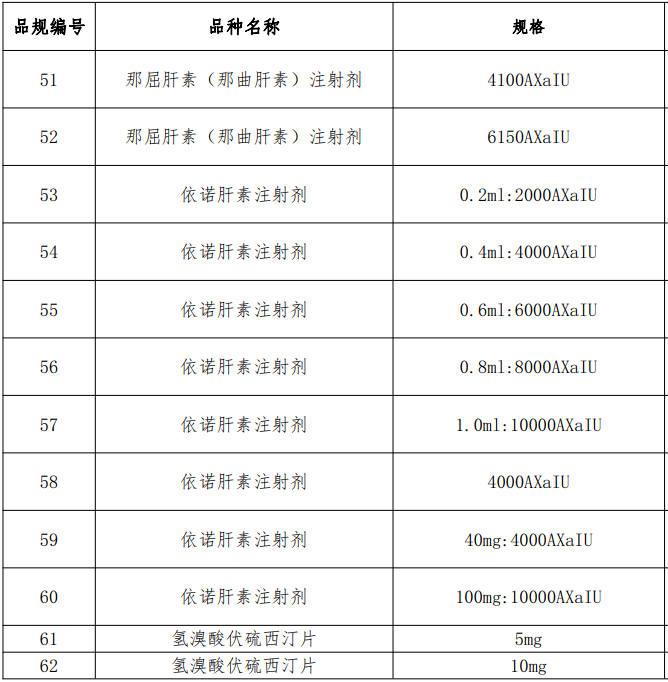

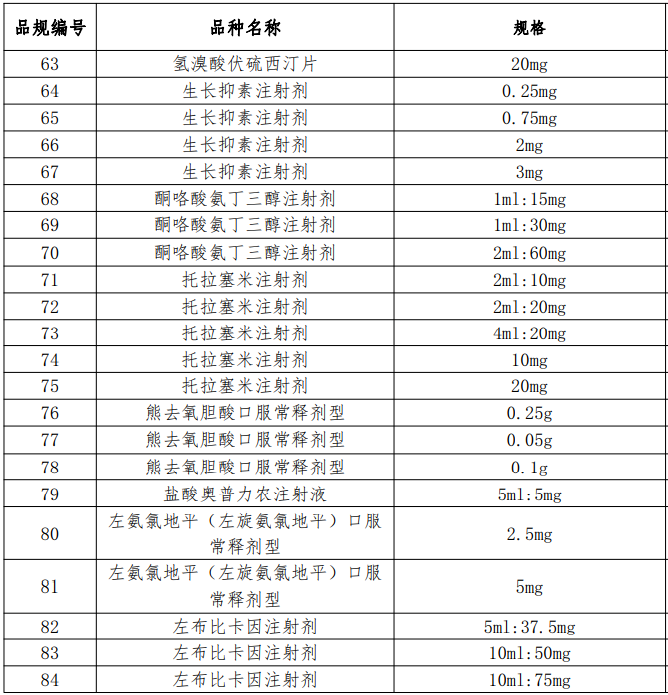

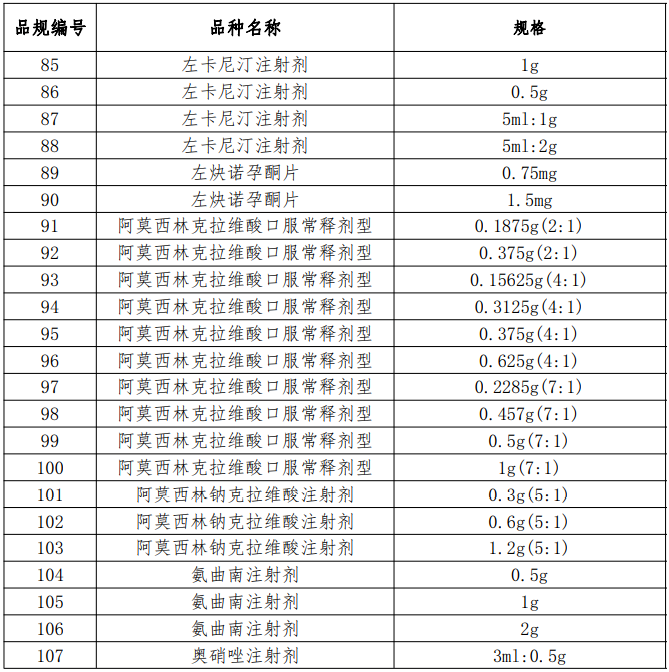

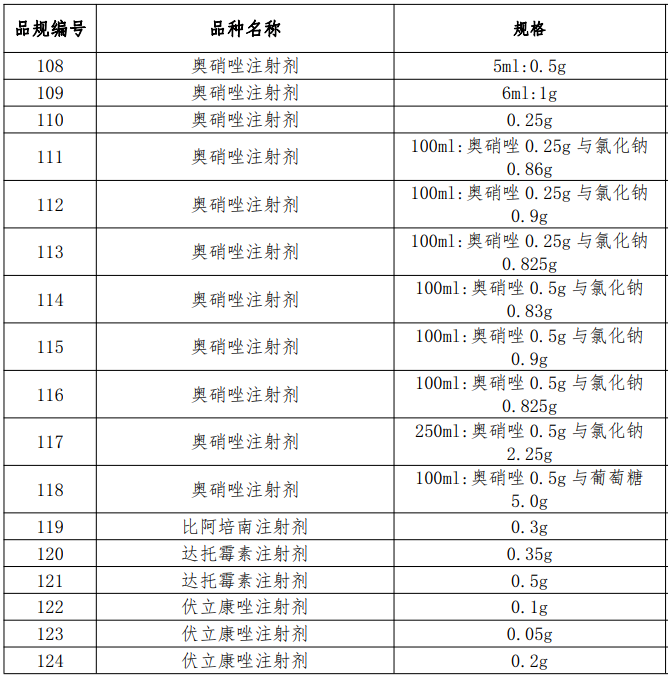

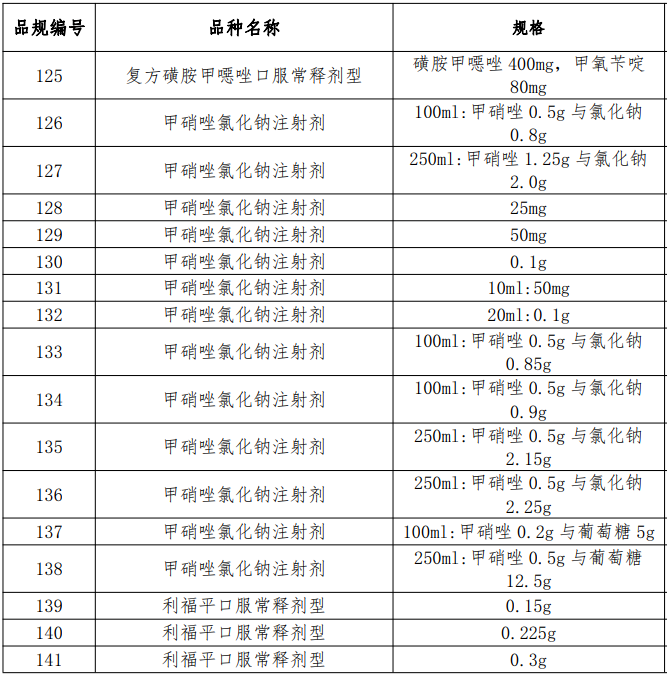

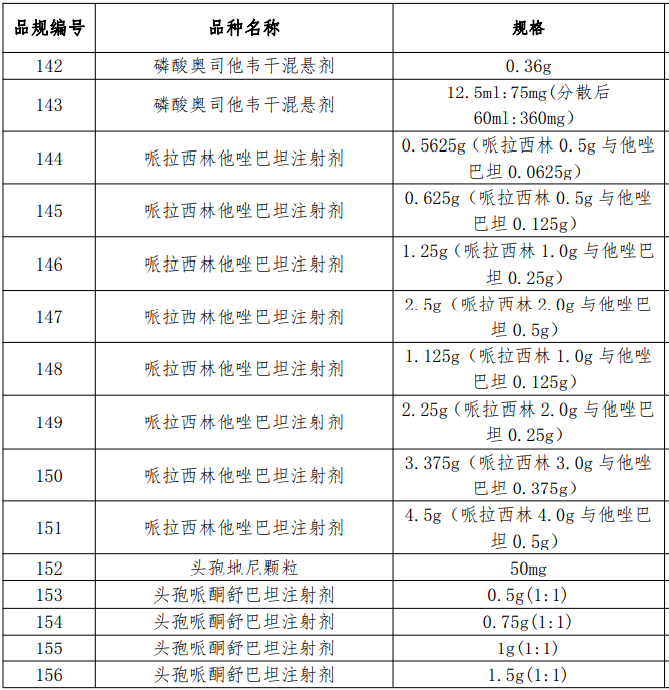

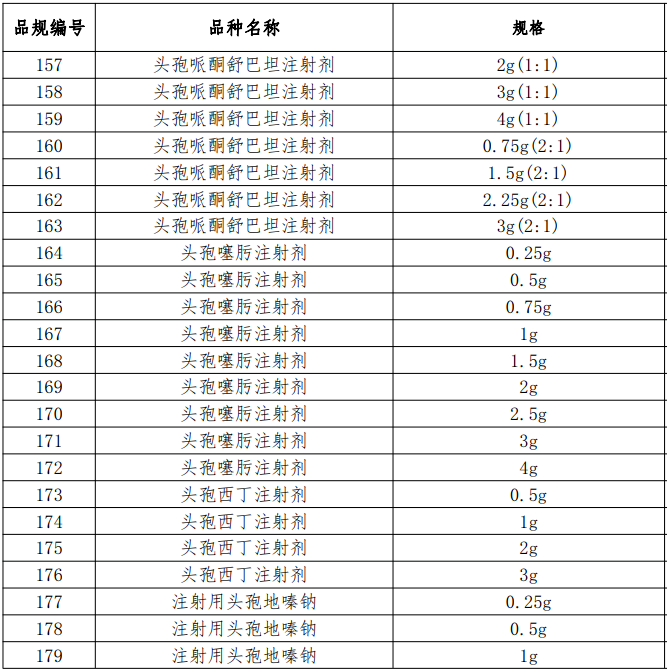

According to publicly available information on the eighth round of centralized procurement, 41 varieties (181 specifications) are planned to be included. Data from Menet show that the total sales of these 41 varieties in China’s public medical institutions in 2021 exceeded RMB 60 billion, with over 20 being blockbuster varieties exceeding RMB 1 billion each. Piperacillin-tazobactam injection leads with over RMB 8 billion in sales; 7 varieties face fierce competition, with 10 or more companies meeting the qualification criteria.

Among multinational originator companies, Pfizer, Sanofi, Merck, Lundbeck, AstraZeneca, and Eisai all have varieties on the list. Pfizer has the highest number of products, with three varieties proposed for inclusion, holding significant market shares for cefoperazone-sulbactam injection and voriconazole injection.

Market analysts indicate that injectable varieties account for over 60% of the eighth round, including several well-known mega-blockbusters. Moreover, the qualification threshold for inclusion has been raised to at least five companies, which will further intensify price competition among bidders. Currently, national centralized procurement has entered a new phase of normalization and institutionalization. Policies are continuously being refined in terms of product pricing and supply security. As procurement reforms deepen, the market remains highly attentive to the evolving impact on the terminal market.

Five Companies Passing Evaluation as Threshold

Competitive Advantages of Leading Companies Highlighted

Based on the publicly available variety list for the eighth round, two main changes are observed: first, the threshold for inclusion has increased from 3+1/4+0 to 4+1/5+0; second, oral solutions are not included in the list. Industry consensus is that raising the threshold from 4 companies in the seventh round to at least 5 means more participating bidders, potentially leading to more intense competition.

Statistics show that among the 41 varieties, 27 are injections, accounting for over 60% of the total. Menet data indicate that injections are the primary route of administration in China’s public medical institutions, consistently accounting for over 50% of the market for many years. In 2021, chemical injections in China’s public medical institutions achieved sales exceeding RMB 600 billion, a year-on-year increase of 10%.

Piperacillin-tazobactam injection leads with sales exceeding RMB 8 billion, with four companies currently having their products pass the generic consistency evaluation. Cefoperazone-sulbactam injection follows closely with sales nearing RMB 7 billion, and seven companies have already passed the evaluation.

In fact, excluding the seventh round’s special insulin procurement, the previous six rounds have included a total of 71 injection varieties (by generic name, with palonosetron injection included in both the fifth and seventh rounds), including major clinical varieties like pantoprazole injection, omeprazole injection, meropenem injection, ceftazidime injection, iodixanol injection, cefuroxime injection, docetaxel injection, and edaravone injection.

From a company perspective, among domestic pharmaceutical companies, Kelun Pharmaceutical, Beite Pharmaceutical, Yangtze River Pharmaceutical Group, North China Pharmaceutical, Qilu Pharmaceutical, China Biopharmaceutical, and Fosun Pharma each have five or more injection varieties involved. Among multinational corporations, Pfizer, Sanofi, and Mitsubishi Tanabe Pharma have multiple injection varieties listed.

Industry analysis suggests that centralized procurement consistently focuses on varieties with “large clinical usage and high procurement value,” ranging from common and chronic disease medications like hypertension, diabetes, digestive system diseases, and immune diseases, to major disease medications such as malignant tumors and rare diseases. Experts note that injections constitute the largest route of administration for systemic antibacterial drugs. As more injectable products pass or are deemed to pass the generic consistency evaluation, it is expected that more systemic antibacterial injections will join the procurement rounds, with an increasing impact on the market.

Among the 41 varieties in the eighth round, 10 domestic companies have five or more varieties that have passed the evaluation. Besides Beite Pharmaceutical, Yangtze River Pharmaceutical Group, Qilu Pharmaceutical, CSPC Pharmaceutical Group, and China Biopharmaceutical, companies like Fosun Pharma, North China Pharmaceutical, China Resources Pharmaceutical, and Lunan Pharmaceutical also have many varieties that have passed the evaluation.

Furthermore, the inclusion threshold has evolved from requiring three companies (including originator) to four, and now to five for the upcoming eighth round. Companies with products that have passed the generic consistency evaluation will all be eligible to participate in price competition, further highlighting the advantages of leading companies in the generic drug sector.

Pfizer Has the Highest Number of Products

Three Products Listed

In November 2018, the fifth meeting of the Central Committee for Deepening Overall Reform reviewed and approved the “Plan for Deepening the Reform of the Government Procurement System.” After over three years of exploration and practice, a system for volume-based procurement has been preliminarily established. Currently, the national volume-based procurement rules are maturing. The scope includes “various drugs with high usage, high value, and clinical necessity.” The main objectives are: 1) reducing drug prices; 2) establishing a drug price formation mechanism; 3) promoting healthcare reform and industrial supply-side reforms.

Over the past three years, China has conducted seven rounds (eight batches) of national centralized drug volume-based procurement. Implementation has expanded from 11 cities to the whole country, and the content has expanded from oral dosage forms to injectable forms, and from chemical drugs to biologics. The variety, quantity, and level of competition have continuously achieved breakthroughs. Procurement rules have also been continuously optimized, quality supervision has become more rigorous, and supply security has become more stable. Overall, the trend has been “price reduction, volume increase, and quality improvement.”

Against the backdrop of centralized procurement, China’s pharmaceutical industry has undergone significant changes. Consequently, multinational pharmaceutical companies are adjusting their strategies and business operations in China, showing gradually increasing enthusiasm for participating in centralized procurement.

Looking back at the seven rounds of national procurement, multinational companies were in a wait-and-see mode during the first round. After the second round, some foreign companies adjusted significantly, actively participating in the expanded procurement with increased price reductions. According to incomplete statistics, over a dozen multinational companies participated in the second round of volume-based procurement, with six foreign companies performing well and winning bids for seven varieties. In the sixth round of insulin national procurement, foreign companies actively competed, with Novo Nordisk, Eli Lilly, Polfa (Poland), and Sanofi having 7, 5, 3, and 2 products respectively proposed as winning bids.

Among the companies involved in the eighth round of centralized procurement, there are over 20 originator drug companies, including multinational corporations such as Pfizer, Sanofi, Merck, Lundbeck, AstraZeneca, and Eisai.

Pfizer has three varieties proposed for inclusion in the procurement list this time, holding significant market shares for cefoperazone-sulbactam injection and voriconazole injection. Menet data shows that in 2020, sales of cefoperazone-sulbactam injection in China’s public medical institutions exceeded RMB 6 billion, with a year-on-year increase of nearly 6% in the first half of 2021. Pfizer holds the largest market share, exceeding 80%. Currently, seven companies, including Suzhou Dongrui Pharmaceutical, Qilu Ante Pharmaceutical, Suzhou Erye Pharmaceutical, and Hainan Herui Pharmaceutical, have passed the consistency evaluation for this product.

Some industry analysts suggest that with the threshold set at five companies for inclusion, more participating bidders may lead to fiercer competition. However, this is favorable for originator and reference-listed drugs that hold a large market share and companies with cost advantages.

Based on current comprehensive information, the bidding is expected to occur about 30 days after the statistical information from the medical insurance administration. Judging from the volume reporting statistics timeline for the eighth round, the bidding is likely to take place around mid-March to early April. The implementation typically follows about four months after the bidding, roughly estimated to be around July or August.

Previous:

Previous: Back to List

Back to List