The expansion of centralized procurement for traditional Chinese medicine (TCM) is accelerating at an ever-faster pace.

On August 15, the Shanghai Sunshine Pharmaceutical Procurement Network issued a notice making arrangements for the city's centralized procurement of TCM patent medicines.

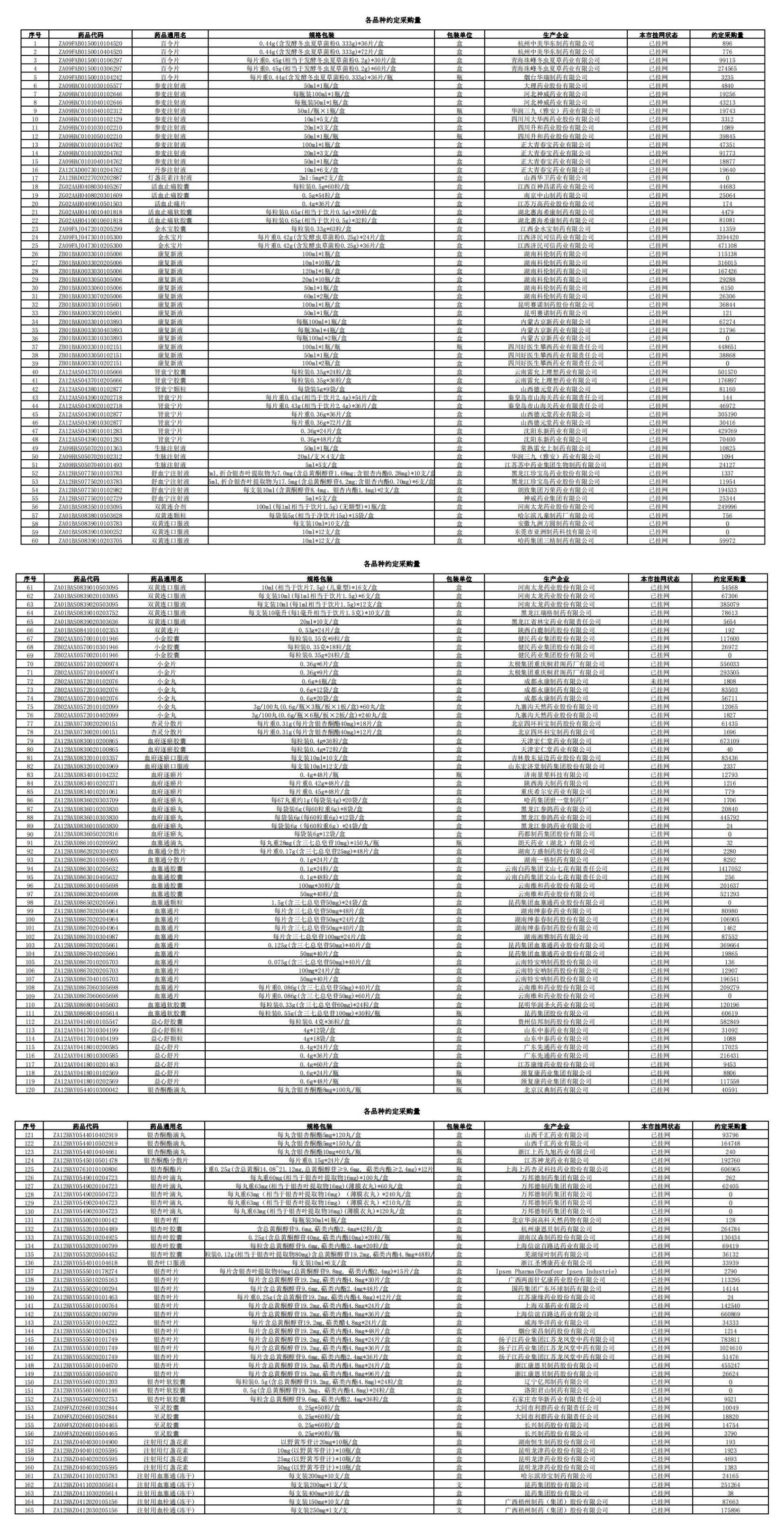

This time, building on the Hubei-led procurement of TCM patent medicines across 19 provinces, Shanghai has included 76 TCM patent medicines in its procurement scope, determining winning enterprises through a volume-based inquiry process. Notably, varieties not yet listed on Shanghai's platform may be included in the procurement, potentially allowing more TCM drugs to enter hospital channels through centralized procurement.

Industry insiders believe that the system and rules for TCM centralized procurement have become increasingly mature. Solutions have been found for challenges such as differences in quality evaluation, the prevalence of exclusive products, and difficulties in bidding and negotiation. Moreover, a procurement framework tailored to the characteristics of TCM has been developed. With the comprehensive advancement of TCM centralized procurement, combined with policies such as rational drug use, healthcare cost control, and medical insurance payment reform, Shanghai’s participation in this round of TCM procurement is conducive to promoting high-quality market upgrades and fostering healthy competition in the industry.

Unlisted Varieties Can Also Participate

Price Competition in Hospital Market

Shanghai’s launch of this TCM volume-based procurement had been foreshadowed.

On August 1, the Shanghai Sunshine Pharmaceutical Procurement Network issued a notice announcing that from August 2 onward, all medical insurance designated medical institutions (including military medical institutions) in Shanghai would begin data reporting for TCM procurement varieties, with a final deadline of August 9. This “volume reporting” move was also seen as a guiding action for further expansion of TCM volume-based procurement.

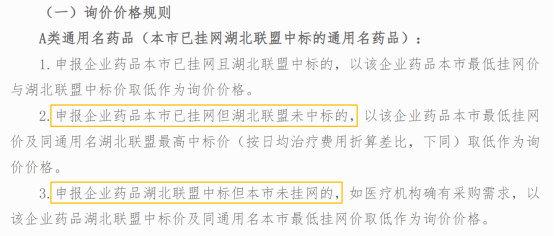

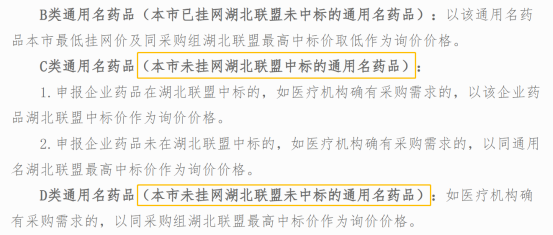

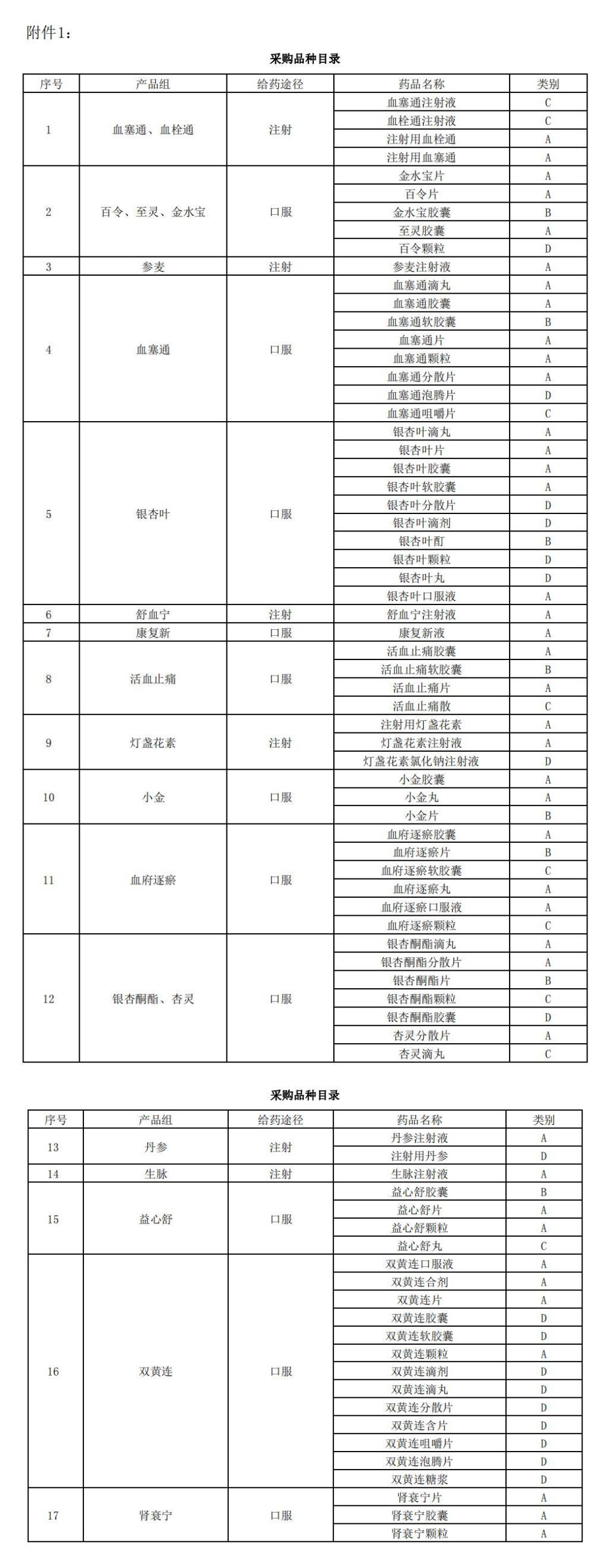

The Shanghai TCM procurement includes both listed and unlisted varieties, with relatively full market competition. Specifically, it covers 17 product groups and 76 products, including blockbuster products such as Xuesaitong, Bailing, Shenmai, Jinshuibao, and Shuxuening, as well as commonly used clinical varieties such as Xuefu Zhuyu, Ginkgo Biloba, Kangfuxin, and Shuanghuanglian. These varieties are generally consistent with those in the Hubei 19-province alliance, and some have appeared in previous TCM centralized procurements in Beijing, the Hubei 19-province alliance, and the Guangdong 6-province alliance. Multiple pharmaceutical companies are involved, including Kun Pharmaceutical, China Resources Sanjiu, Leiyunshang, and Kelun. (See the end of the article for the complete procurement variety list.)

Notably, 164 specifications from 99 companies are already listed in Shanghai. Hunan Kelun and Wanbangde Pharmaceutical have 6 and 5 specifications, respectively; Tailong, Weihe, and Zhengda Qingchunbao each have 4 specifications listed. From a product perspective, Kangfuxin Liquid, Ginkgo Biloba Tablets, Xuesaitong Tablets, and Shenmai Injection all have multiple specifications and manufacturers listed.

Taking Ginkgo Biloba Tablets as an example, the current exclusive supplier in Shanghai is Sinopharm Group Guangdong Global Pharmaceutical Co., Ltd. Manufacturers of the same product not yet listed include Zhongjing Wanxi, Conba, Anhui Shengying, and Jiangsu Chenpai. Hundreds of unlisted varieties exist for Xuesaitong Dispersible Tablets and Shuanghuanglian Oral Liquid.

Against this backdrop, Shanghai’s procurement adopts a unique rule: medical institutions are allowed to report procurement needs for unlisted varieties or varieties not selected in the Hubei alliance procurement, provided they explain reasonable grounds for participation. Industry observers widely believe that Shanghai’s decision to give unlisted companies an opportunity to apply will encourage companies to compete on price to gain access to the hospital market.

Meanwhile, the participating institutions in this centralized drug procurement are all medical insurance designated medical institutions in Shanghai (including military medical institutions), with other medical institutions encouraged to voluntarily participate. The agreed procurement volume is 80% of the total procurement demand reported by all participating medical institutions. If a medical institution does not report demand, the first-year agreed procurement volume is zero.

Under the requirements of this volume-based procurement, if the agreed procurement volume is completed ahead of schedule during the procurement cycle, the winning enterprise must continue to supply the excess at the winning price until the cycle ends. If the national government organizes centralized procurement for the same drug during the procurement cycle, the transition will be handled in accordance with national policies.

Shanghai Follows Hubei 19-Province Alliance

TCM Centralized Procurement Becomes a Trend

The National Healthcare Security Administration’s “Notice on the Work of Centralized Drug Procurement and Price Management in 2023” outlined priorities for the year’s pharmaceutical procurement efforts, emphasizing the continued expansion of drug procurement coverage. By the end of 2023, the total number of drugs procured through national and provincial centralized procurement in each province should reach 450, including 130 at the provincial level, covering chemical drugs, TCM, and biologics.

To date, the state has organized the procurement of 294 drugs, with an average price reduction of over 50% for a range of common outpatient and chronic disease medications such as those for hypertension, coronary heart disease, and diabetes. Thanks to significant price reductions, the proportion of patients using high-quality drugs has increased from 50% before procurement to over 90%.

In fact, although the national government has not organized TCM centralized procurement, provincial-level procurement has been frequent, making TCM centralized procurement a clear trend:

On December 21, 2021, Hubei led the first large-scale centralized procurement of TCM across 19 provinces and regions. At that time, the procurement catalog involved 17 product groups with 157 companies and 182 products participating. Through on-site competition, 97 companies and 111 products were selected, with a selection rate of 62%, an average price reduction of 42.27%, and a maximum reduction of 82.63%. This was, at the time, the largest-scale TCM centralized procurement to date, aside from drug, device, and other specialized procurements.

On April 8, 2022, Guangdong “took the baton” from Hubei, launching its own TCM centralized procurement. In this round, 124 manufacturers were selected, with 56 entering the preliminary backup list. Companies such as Baiyunshan, Shenwei Pharmaceutical, Xiangxue Pharmaceutical, Tasly, Kelun Pharmaceutical, Panlong Pharmaceutical, Yiling Pharmaceutical, and China Resources Sanjiu all had products provisionally selected. The provisional selection/backup rates for companies and products were 63.27% and 62.67%, respectively, with an overall average price reduction of 56% for selected varieties, a maximum reduction of 99%, and a minimum reduction of 1%.

On June 21, 2023, Hubei led a TCM alliance procurement covering 30 provinces and cities, involving 16 varieties. A total of 63 companies and 68 quoted varieties were selected. According to data released by the National TCM Joint Office, selected prices for various drugs decreased to varying degrees, with a maximum reduction of 98% and an average reduction of 49.36%. Based on estimated annual procurement amounts in the 30-province alliance region, annual drug cost savings are expected to exceed RMB 4.5 billion.

Industry observers believe that under the influence of price radiation within the hospital market, overall TCM prices may trend downward in the future. Drug procurement has now extended from chemical drugs to TCM, with a broader scope. Based on past experience with provincial TCM centralized procurement, compared with chemical drugs, TCM procurement has been relatively moderate in terms of price reductions. Chemical drug procurement has averaged reductions of over 50%, reaching as high as 90%, while TCM reductions have generally remained in the 30%–40% range.

This year, following the announcement of the national TCM centralized procurement results, provinces have successively begun selecting and confirming their agreed procurement volumes. Hubei, Beijing, and Henan have already issued relevant notices, with the target selection process to be completed by August 8.

Industry experts believe that, judging by the timing of the results announcement, the Hubei 19-province TCM alliance procurement was the country’s first such alliance. Its approaches, such as grouping products together, provided valuable experience for subsequent rounds of TCM procurement. Shanghai’s decision to follow the Hubei 19-province TCM procurement in August, explicitly using the “Hubei alliance winning price” as a competitive threshold in its bidding rules, sends a very strong signal of the expanding and advancing nature of TCM centralized procurement.

Against the backdrop of rising prices for upstream Chinese herbal medicines, TCM drug prices are trending downward. Price and cost pressures are comprehensively testing the capabilities of enterprises. In reality, centralized procurement presents both opportunities and challenges for TCM companies. Market analysts suggest that on the one hand, procurement will inevitably reduce TCM sales prices, further compressing corporate profit margins. Companies with a large hospital market share should avoid losing bids, while those with a smaller market presence can seize the opportunity to enter.

On the other hand, national procurement also serves as an opportunity to drive industrial transformation and upgrading, encouraging TCM companies to increase R&D investment and advance new drug development. Facing this new landscape, companies must focus on developing products with significant market potential and high R&D barriers, or prioritize exclusive products to seek differentiation and competitive advantage.

Posting Date:2023-08-18

Posting Date:2023-08-18 Views:

Views:

Previous:

Previous: Back to List

Back to List