Copyright © 2025 Shenyang Dasan Pharmaceutical Technology Co., Ltd.

Posting Date:2022-07-01

Posting Date:2022-07-01 Views:

Views:

On May 9, the "Implementing Regulations of the Drug Administration Law of the People's Republic of China (Revised Draft for Comments)" (referred to as the "Draft for Comments") issued by the National Medical Products Administration completed its one-month public comment period. Among the additions, Article 83 explicitly stipulates that third-party platform providers shall not directly participate in online drug sales activities.

This policy change reverberated through the secondary market, causing significant declines in related pharmaceutical e-commerce stocks and attracting public attention. The topic "State proposes to ban third-party platforms from directly participating in online drug sales" trended on Weibo, with views exceeding 100 million.

Many netizens expressed concerns about future online drug purchases. It is important to note that this Draft for Comments does not involve "halting" online drug sales and has no impact on consumers buying drugs online. The focus is on "who can sell drugs online and how they can participate."

As online drug sales become normalized and the scale of third-party platform drug retail markets expands, some pharmaceutical e-commerce platforms operate both self-operated businesses and host third-party sellers. Based on the Draft for Comments, the National Medical Products Administration aims to further clarify the boundaries between these two types of operations.

Although this may concern the future of e-commerce platforms' self-operated businesses, taking JD Health and Ali Health as examples, their self-operated segments are backed by offline physical pharmacies, currently meeting the proposed requirements. Ping An Good Doctor responded to TMTPost, stating that the company has initiated study, research, and strict self-inspection, and will continue to enhance and strengthen its medical service levels in accordance with policy requirements in the future.

What exactly is the Draft for Comments that has shaken the industry?

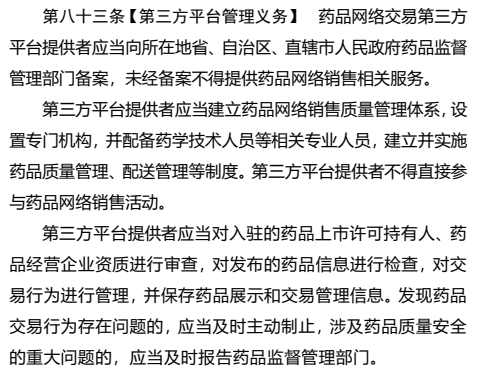

This Draft for Comments adds regulatory provisions for third-party platforms in online drug transactions, concerning how these platforms can participate in online drug sales. Article 83, "Management Obligations of Third-Party Platforms," explicitly mentions three points:

1. Providers of third-party platforms for online drug transactions must register with the drug regulatory authority of the province, autonomous region, or municipality directly under the central government where they are located. Those not registered may not provide services related to online drug sales.

2. Third-party platform providers shall establish a quality management system for online drug sales, set up specialized agencies, employ pharmaceutical technologists and other relevant professionals, and establish and implement systems for drug quality management and distribution management. Third-party platform providers shall not directly participate in online drug sales activities.

3. Third-party platform providers shall verify the qualifications of drug marketing authorization holders and drug distributors settled on their platforms, inspect the drug information published, manage transaction activities, and retain drug display and transaction management information. If issues are found with drug transactions, they shall promptly intervene, and for major issues related to drug quality and safety, they shall promptly report to the drug regulatory authority.

Overall, as the online closed-loop of medical services gradually improves, pharmaceutical e-commerce, as a key component, has grown significantly. Pharmaceutical e-commerce offers multiple advantages, including broad user reach, significant economies of scale, and strong bargaining power. The "Measures for the Supervision and Administration of Online Drug Sales (Draft for Comments)" released in 2020 promoted the liberalization of prescription drug sales online, with policies strongly supporting the development of pharmaceutical e-commerce.

Under the dual influence of favorable policies and the catalyst of the pandemic, China's pharmaceutical e-commerce market transaction size surged in 2020, surpassing the 200 billion yuan mark the following year to reach 223 billion yuan. Pharmaceutical e-commerce also overtook primary healthcare to become the fourth-largest retail terminal. However, hospitals and physical pharmacies remain firmly in the top two positions among the four major retail terminals.

Facing a larger market, regulators are also seeking to establish reasonable market entry barriers. This Draft for Comments emphasizes the registration requirements for third-party platform providers and the establishment of drug sales quality management systems. It also imposes requirements for reviewing drugs from settled entities, managing transactions, and handling safety issues. Beyond these routine strict regulations, it explicitly states that "third-party platform providers shall not directly participate in online drug sales activities," which has drawn widespread attention.

What is a "third-party platform"?

The "Measures for the Supervision and Administration of Online Drug Sales (Draft for Comments)" stipulates that a provider of a third-party platform for online drug transactions refers to a legal entity or unincorporated organization that provides services such as online marketplace, transaction matching, and information publishing for two or more parties to conduct transaction activities in online drug transactions.

Additionally, engaging in online drug sales or providing third-party platform services for online drug transactions requires possessing appropriate qualifications or conditions, complying with drug laws, regulations, rules, and standards, operating with integrity and in accordance with the law, and ensuring drug quality and safety.

Currently, the main participants in pharmaceutical e-commerce include pharmaceutical B2C and pharmaceutical O2O platforms. Major representatives of the former include JD Health, Ali Health, Ping An Health, and 1 Drug Network, while the latter include Ele.me, Meituan, Dingdang Health, and Kuaifang Songyao. These are all considered third-party platforms.

Furthermore, how should "direct participation" be understood?

Current pharmaceutical e-commerce players operate both self-operated and non-self-operated business models. For example, Tmall Medical under Ali Health, JD Big Pharmacy under JD Health, 111 Medical under 1 Drug Network, and the self-operated pharmacy under Ping An Health all constitute self-operated segments. In contrast, platforms like Meituan and Ele.me only provide services for pharmacies to list on their platforms, without engaging in self-operated related businesses. Some industry insiders suggest that "direct participation" likely targets the self-operated businesses of pharmaceutical e-commerce platforms.

The policy has not yet been finalized, and the market need not rush to judgment.

However, based on the wording of this Draft for Comments, some degree of interpretation discrepancy exists.

Some industry insiders point out that the Draft for Comments has led to market misunderstanding that third-party platforms for drug transactions cannot operate both third-party and self-operated businesses. In reality, for most platforms, third-party and self-operated businesses are managed by different companies. If the new regulation is implemented, its impact on companies and the industry is expected to be limited.

In this regard, Northeast Securities stated that if this regulation is strictly enforced, the self-operated operations of pharmaceutical e-commerce might be affected, but the overall impact would be limited. Currently, self-operated e-commerce platforms all operate using the qualifications of offline pharmacy chains. Ali Health's offline entity is "Guangzhou Wunian Pharmaceutical," and JD Health's is "Qingdao Ajitang Pharmacy." If the policy is strictly enforced, it is possible that self-operated e-commerce platforms might spin off independent companies to operate their self-operated businesses separately.

In terms of feasibility, although spinning off self-operated businesses for independent operation is a "way out," self-operated businesses inherently have high operating costs, including warehousing, logistics, customer service, and related personnel expenses. If a platform relies solely on self-operation, it would only worsen the already thin gross margins of e-commerce platforms.

It is important to note that while the development of the pharmaceutical e-commerce industry has impacted offline pharmacies, looking at future trends, as consumers are attracted to online retail pharmacies, an increasing number of offline pharmacies are seeking cooperation with online channels. This has led to market concerns about e-commerce platforms "acting as both referee and player," especially since major third-party platforms command significant industry traffic.

Therefore, as potential beneficiaries of the news, pharmaceutical O2O platforms and offline pharmacy chains saw significant gains.

Previous:

Previous: Back to List

Back to List