Copyright © 2025 Shenyang Dasan Pharmaceutical Technology Co., Ltd.

Posting Date:2022-07-29

Posting Date:2022-07-29 Views:

Views: On July 26, the National Healthcare Security Administration and the Ministry of Finance issued the "Notice on Further Improving the Direct Settlement Policy for Inter-provincial Cross-region Medical Treatment under Basic Medical Insurance." This notice aims to deepen the reform of direct settlement for inter-provincial cross-region medical treatment under basic medical insurance. It requires local healthcare security departments to promptly adjust any policies and measures inconsistent with this notice, ensuring alignment with the national policy by the end of December 2022.

The Notice stipulates that for inpatient services, general outpatient services, and outpatient services for chronic and special diseases covered by inter-provincial direct settlement, the scope of payment and relevant regulations of the medical treatment location shall apply in principle. Meanwhile, the policies of the insured location, including the deductible, reimbursement ratio, maximum reimbursement limit, and the scope of chronic and special diseases covered, shall also apply. The "Procedures for Inter-provincial Cross-region Direct Settlement under Basic Medical Insurance" will be officially implemented on January 1, 2023.

This means that starting next year, insured individuals who are long-term residents outside their insured province or who seek temporary medical treatment outside their insured province will be able to access direct settlement services for inter-provincial medical treatment after completing the necessary registration. The settlement will follow the directory of the medical treatment location and the policies of the insured location.

Industry experts point out that with increasingly frequent population mobility, the number of scenarios involving cross-region medical treatment will continue to grow. In the past, the existence of provincial-level medical insurance directory supplementation systems led to a long-standing inconsistency between provincial and national directories, posing challenges to direct settlement for cross-region medical treatment. Now that the nationally unified medical insurance information platform has been established, and the countdown to the removal of provincial-level medical insurance directory drugs has begun, the 'national coordination' of the medical insurance directory will undoubtedly accelerate the reshuffling of provincial-level regional drug markets. In the future, if a drug fails to be included in the national medical insurance directory, the 'window' of opportunity in provincial markets will cease to exist.

Medical Insurance Directory Achieving "National Coordination"

Major Local Drug Varieties in Jeopardy

China's vast territory leads to significant disparities in economic development levels and medical conditions across regions. Consequently, medical insurance policies, reimbursement directories, and reimbursement ratios vary among provinces and cities. This historical issue creates a "mismatch" with the growing demand for cross-region medical treatment, causing considerable inconvenience for the public in seeking medical reimbursement.

Initially, allowing provincial-level supplementations was intended to accommodate local prescribing habits. However, during implementation, issues such as protecting the interests of local pharmaceutical companies became unavoidable. Furthermore, the time lag between adjustments to provincial directories and the national directory in the past also prevented medical insurance agencies from settling the full amount.

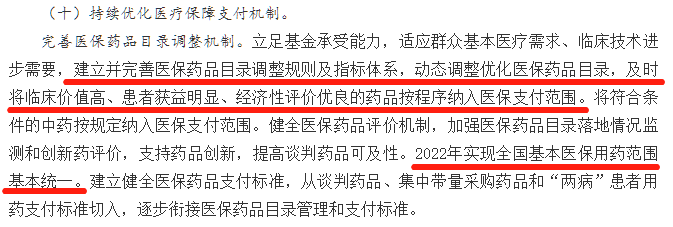

To ensure that medical insurance funds are used effectively, it is imperative to promote the unification of the national medical insurance directory. In September 2021, the General Office of the State Council issued the "14th Five-Year Plan for National Medical Security," which explicitly set the goal of achieving a basically unified scope of basic medical insurance drug coverage nationwide by 2022, and to establish a sound payment standard for medical insurance drugs. By 2025, the medical security system is expected to become more mature and well-defined, with significantly enhanced information technology capabilities. Looking ahead to 2035, the basic medical security system is envisioned to be more standardized and unified, the multi-tiered medical security system more comprehensive, the public medical security service system more robust, and a collaborative governance structure among medical insurance, medical services, and pharmaceuticals generally formed.

In May 2022, the General Office of the State Council issued the "Notice on Issuing the Key Tasks for Deepening the Reform of the Medical and Health System in 2022," once again emphasizing the need to achieve a basically unified scope of medical insurance drug coverage nationwide.

According to the National Healthcare Security Administration's regulations, all localities must strictly implement the "2021 Drug Directory" and are not permitted to adjust the reimbursement restrictions or the Category A/B classification of drugs listed in the directory on their own. Provincial-level healthcare security departments must accelerate the removal of previously self-supplemented drugs, ensuring completion by June 30, 2022.

June 30, 2022, was the final deadline for provinces to adjust their locally supplemented medical insurance drugs. So, how have the provinces performed?

Recently, a relevant official from the Medical Service Management Department of the National Healthcare Security Administration stated publicly to the media that 15 provinces and the Xinjiang Production and Construction Corps completed the task of "removing" all locally supplemented drugs ahead of schedule. The remaining 16 provinces, including Beijing, are set to complete the "removal" of these drugs by the end of this year. In other words, by the end of 2022, all provinces across the country will have completed the removal of locally supplemented drugs, achieving a basically unified scope of medical insurance drug coverage nationwide.

Given the complexity of phasing out provincial-level supplemented directories, the National Healthcare Security Administration arranged a three-year transition period. Starting from 2020, localities were required to gradually phase out the Category B drugs that had been added to their original provincial drug directories over three years, following a ratio of 40% in the first year, 40% in the second year, and 20% in the third year. Among these, drugs under monitoring for auxiliary use were prioritized for removal.

There is a broad consensus in the industry that the unification of the national medical insurance directory will make cross-region medical treatment more convenient, improve administrative efficiency, and better reflect the fairness of medical insurance. Moreover, with the nationwide unified medical insurance information platform now operational, the standardized management of drugs within the medical insurance directory will also be strengthened. In the future, for a drug to enter the medical insurance payment system, inclusion in the national medical insurance directory will become the only pathway.

In fact, inclusion in the medical insurance directory is one of the primary drivers for increasing drug sales. Being removed from the directory will lead to a significant decline in sales for the relevant products. The more provinces a drug had been supplemented into, the greater the impact it will face upon removal.

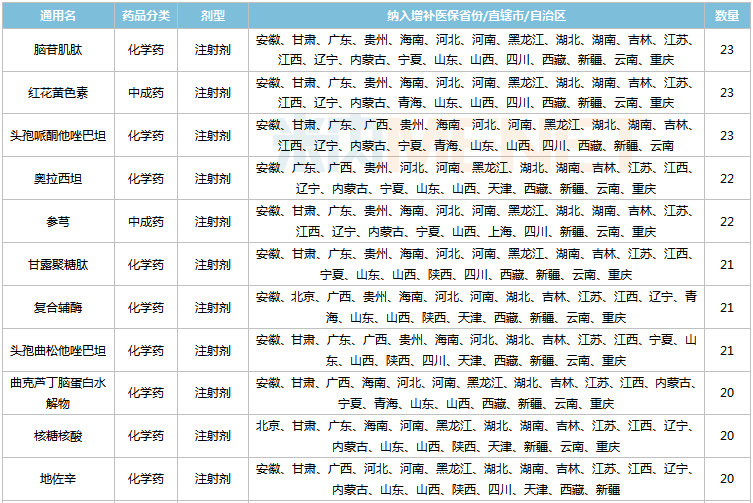

As provincial medical insurance directories gradually fade out, many major drugs previously covered by local medical insurance now face the risk of becoming out-of-pocket expenses. The consequent market impact is可想而知. According to data from Mnet, excluding varieties already included in the national medical insurance directory, 41 varieties were supplemented in 15 or more provinces and cities. Among these, 35 were chemical drugs and 6 were traditional Chinese patent medicines.

Varieties Supplemented into Category B Medical Insurance in 15 or More Provinces and Cities

Source: Mnet China Medical Insurance Directory Database

Among these varieties, 13 products, including Cattle Encephalon Glycoside and Ignotin Injection, Cefoperazone and Tazobactam Injection, Oxiracetam Injection, Yanhuning Injection, Ganglioside Injection, Thymopentin Injection, Creatine Phosphate Sodium Injection, Sodium Potassium Magnesium Calcium Glucose Injection, Cefodizime Injection, Rhodiola Injection, and Cefamandole Injection, each achieved sales revenue exceeding 1 billion yuan in China's public medical institution terminal market in 2020.

"Ineffective Drugs" Are Bound to Be Phased Out

"Value-Based Healthcare" Drives Transformation for Pharmaceutical Companies

As medical insurance payment reforms deepen, initiatives like volume-based procurement and医保 negotiations aim to "replace the old with the new," focusing on "major varieties" with high clinical usage and high expenditure. After provincial directories leave the stage, products not included in the national directory will have to seek transformation opportunities in out-of-hospital markets or self-pay markets, inevitably facing immense performance pressure.

The "countdown" to the removal of provincial-level medical insurance drugs has already impacted some major clinical drug varieties. On June 28, Jumpcan Pharmaceutical announced that varieties including its wholly-owned subsidiary's Pudilan Xiaoyan Oral Liquid and Iron Protein Succinylate Oral Solution would be removed from multiple provincial medical insurance directories effective June 30, 2022.

It is understood that in 2021, the sales amount of Pudilan Xiaoyan Oral Liquid in Jiangsu Province, Hunan Province, Jilin Province, Qinghai Province, and Tianjin City was approximately 700 million yuan; the sales amount of Iron Protein Succinylate Oral Solution in Jiangsu and Hunan provinces was approximately 100 million yuan.

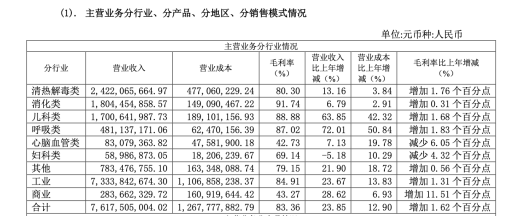

As a flagship product, Pudilan Xiaoyan Oral Liquid is Jumpcan Pharmaceutical's exclusive formulation. Since its launch in 2013, its cumulative sales have exceeded 10 billion yuan, ranking first among oral traditional Chinese medicines for heat-clearing and detoxifying for many consecutive years. According to its 2021 annual report, Jumpcan Pharmaceutical achieved a revenue of 7.631 billion yuan, of which the heat-clearing and detoxifying category, to which Pudilan Xiaoyan Oral Liquid belongs, achieved a revenue of 2.422 billion yuan, contributing over 30% of the total revenue.

However, according to a research report by Southwest Securities, by 2021, the proportion of Pudilan Xiaoyan Oral Liquid's revenue relative to the company's total revenue had decreased from 44.3% in 2018 to 34.7%.

Facing the pressure of its flagship product being removed from the medical insurance directory and the risk of declining sales, Jumpcan Pharmaceutical is continuously exploring ways to boost performance. At its 2020 performance briefing, Jumpcan Pharmaceutical's Chairman Cao Longxiang stated that the company was vigorously developing its daily chemicals business. In 2021, Jumpcan Pharmaceutical also indicated on public platforms that it would subsequently establish connections with e-commerce platforms to expand its market.

Industry insiders suggest that there are already many daily chemical brands available in the market. Compared to companies specializing in daily chemicals, pharmaceutical companies have relatively weaker advantages in terms of channels and distribution. In fact, the performance contribution from daily chemicals to Jumpcan Pharmaceutical is not substantial. In 2021, the revenue of Jiangsu Pudilan Daily Chemical Co., Ltd., the entity operating Jumpcan's daily chemical business, was 93.048 million yuan.

For a company entering the highly competitive daily chemical market without prior experience, capturing a certain market share is no easy task. Jumpcan Pharmaceutical, which heavily relies on Pudilan Xiaoyan Oral Liquid, has a long way to go.

Another product facing a similar fate is Guizhou Baite's Salvia Miltiorrhiza and Ligustrazine Injection.

In 2019, Salvia Miltiorrhiza and Ligustrazine Injection was included in the national list of key monitored drugs. Concurrent with the National Healthcare Security Administration's issuance of the "Opinions on Establishing a Management System for Medical Insurance Treatment Lists (Draft for Comments)," the product was removed from provincial-level medical insurance payment directories in 2020.

Following this, the sales of Salvia Miltiorrhiza and Ligustrazine Injection plummeted. Its sales value dropped from 1.783 billion yuan in 2018 to 1.411 billion yuan in 2019, and net profit fell from 373 million yuan to 284 million yuan. Considering inventory, expected market channel and terminal stock usage progress, Guizhou Baite suspended production of Salvia Miltiorrhiza and Ligustrazine Injection in December 2019.

In January 2021, Guizhou Baite applied to the drug regulatory authority for production suspension and filed a record. To reduce operating costs and potential ongoing losses stemming from operational uncertainty, the drug registration approval for Salvia Miltiorrhiza and Ligustrazine Injection was revoked on February 23, 2021.

In the era of "value-based healthcare," focusing on unmet clinical needs is paramount. Good products are always those urgently needed in clinical practice. Regular adjustments to the national medical insurance directory will become the sole pathway for pharmaceutical companies to gain access.

Experts suggest that from the policy adjustments at both the policy-making and payment ends, it is evident that pharmaceutical companies focused solely on sales have no future. For companies whose products are being removed from provincial-level supplemented medical insurance lists, one path forward is to conduct secondary development to verify the drug's efficacy and safety, striving for inclusion in the national medical insurance directory. Simultaneously, they must be psychologically prepared for significant price reductions.

For pharmaceutical companies, building a professional promotional team and investing in post-marketing clinical re-evaluation require a sufficiently long-term strategic vision. Whether targeting the medical insurance market or the self-pay market, being guided by clinical value, adhering to innovation-driven high-quality development, and enhancing capabilities in full-cycle product quality management and brand service awareness will be crucial for future success.

Previous:

Previous: Back to List

Back to List