Copyright © 2025 Shenyang Dasan Pharmaceutical Technology Co., Ltd.

Posting Date:2023-06-09

Posting Date:2023-06-09 Views:

Views: The market size of China's antihypertensive drug industry has been growing steadily, exceeding RMB 100 billion in 2021 to reach RMB 103.5 billion, a year-on-year increase of 8.26%.

Recently, the National Medical Products Administration (NMPA) approved the marketing of urapidil hydrochloride injections, generic versions from Shijiazhuang No.4 Pharmaceutical and Jiangxi Qingfeng Pharmaceutical. Urapidil hydrochloride injection is a first-line treatment for hypertensive emergencies. It is widely used in clinical practice for various antihypertensive treatments, including hypertensive crisis, blood pressure management during surgery, and prevention of blood pressure spikes. It is a highly selective α-receptor blocker. According to data from Zhongkang CMH, its sales in hospital settings reached RMB 1.099 billion in 2022.

To date, seven companies hold production approvals for urapidil hydrochloride injection: the originator, Takeda Pharmaceutical, and generic manufacturers including Shijiazhuang No.4 Pharmaceutical, Qingfeng Pharmaceutical, Luoxin Pharmaceutical, Aohong Pharmaceutical, Yipin Pharmaceutical, and Lijun Pharmaceutical. Additionally, several other companies have filed for production approval, which are currently under review.

01. China Currently Has 333 Million Hypertensive Patients; Market Expected to Exceed RMB 142 Billion Within Two Years

Hypertension is one of the leading and most common causes of cardiovascular disease mortality and hospitalization. Evidence shows that cardiovascular diseases such as stroke and myocardial infarction are correlated with elevated blood pressure, significantly impacting people's health and well-being.

From 2016 to 2022, the number of people with hypertension in China increased from 297 million to 333 million. According to the China Hypertension Annual Conference held on March 11 this year, the prevalence of hypertension in China has generally shown an upward trend in recent years, with a notable increase among the middle-aged and young adult populations. The weighted prevalence of hypertension among adults aged 18 and above in China is 27.5%.

The market size of China's antihypertensive drug industry has been growing steadily, exceeding RMB 100 billion in 2021 to reach RMB 103.5 billion, a year-on-year increase of 8.26%. It continues to maintain a relatively high growth rate. With the accelerating trend of population aging in China, the market size of antihypertensive drugs is expected to continue rising, projected to exceed RMB 142 billion by 2025.

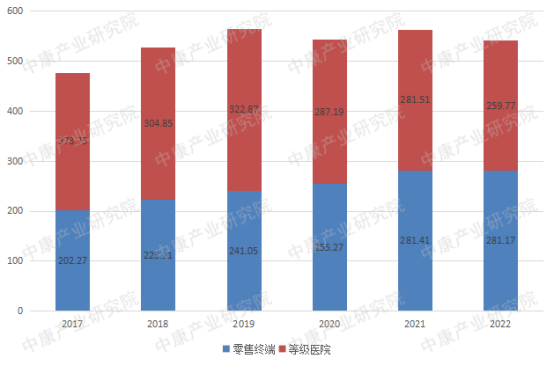

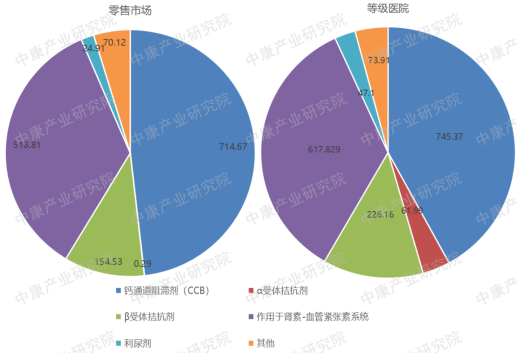

The market size for antihypertensive drugs is substantial in both retail and hospital settings, with sales reaching tens of billions of RMB in each channel. Looking at sales from 2017 to 2022, calcium channel blockers accounted for half of the market, followed by drugs acting on the renin-angiotensin system. β-blockers and α-blockers had smaller sales volumes compared to the first two categories.

Figure 1: Sales of Antihypertensive Drugs by Category (2017-2022, RMB billion)

Figure 2: Sales of Antihypertensive Drugs by Sub-Category (2017-2022, RMB billion)

02. Hospital Performance of Five Common Antihypertensive Drug Classes: Nifedipine, Metoprolol, Felodipine Top the List

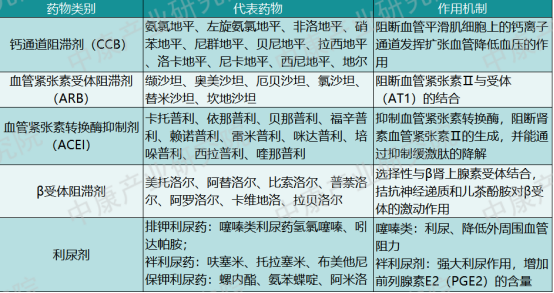

Currently, guidelines recommend five main classes of antihypertensive drugs for clinical use: calcium channel blockers (CCBs), angiotensin II receptor blockers (ARBs), angiotensin-converting enzyme inhibitors (ACEIs), β-blockers, diuretics, and single-pill combinations (SPCs) of the above. Table 1 lists representative drugs under each category. α-blockers are not listed here, as the focus is on the first-line drug classes recommended by guidelines.

Table 1: Categories of Antihypertensive Drugs

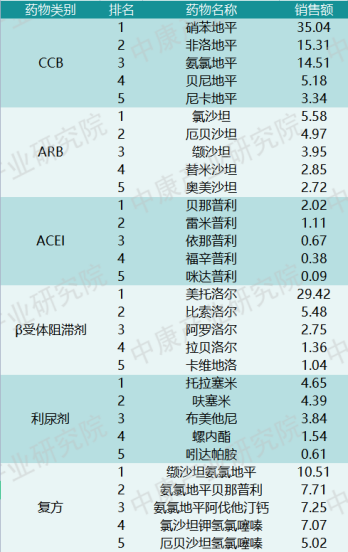

According to the 2022 sales ranking of antihypertensive drugs in domestic hospital settings, CCBs and their combination formulations were the most mainstream, achieving the highest sales.

Figure 3: Top 15 Antihypertensive Drugs by Sales in Domestic Hospital Settings (2022)

Breaking down by drug class, Table 2 lists the top 5 drugs by sales in hospital settings for each category in 2022. It can be seen that nifedipine and metoprolol are major products in the antihypertensive market, with sales reaching tens of billions of RMB. Combination formulations are typically used for resistant hypertension or hypertension accompanied by other conditions.

Table 2: Top 5 Antihypertensive Drugs by Sales in Hospital Settings, by Category (2022, RMB billion)

03. "Rising Star" Entresto Shines Bright; Multiple Domestic Companies Vie for "First Generic"

The 2023 hypertension guidelines added angiotensin receptor-neprilysin inhibitors (ARNIs) as a new class of commonly used antihypertensive drugs. Sacubitril/valsartan is the first ARNI drug, with its primary hypertension indication approved by the NMPA in 2021.

Evidence suggests that this drug offers certain advantages over other classes in specific patient populations, including those with diabetes, heart failure, kidney disease, and resistant hypertension. Its unique co-crystal structure balances drug stability, bioavailability, safety, and side effects, providing a new basis for first-line hypertension treatment. This drug holds significant potential for future clinical application.

In mainland China, sacubitril/valsartan is only available as an imported product (Entresto), with the originator, Novartis, being the sole approved manufacturer. The drug has been included in the national reimbursement drug list. In 2022, sales of sacubitril/valsartan in domestic hospital and retail settings reached RMB 2.127 billion and RMB 743 million respectively, representing a substantial market size. With its inclusion in the guideline-recommended drugs, it is expected to experience further growth.

Currently, around 20 companies are actively vying to be the first to launch a generic version, having submitted marketing applications. These include Chia Tai Tianqing, Qilu Pharmaceutical, and Kelun Pharmaceutical.

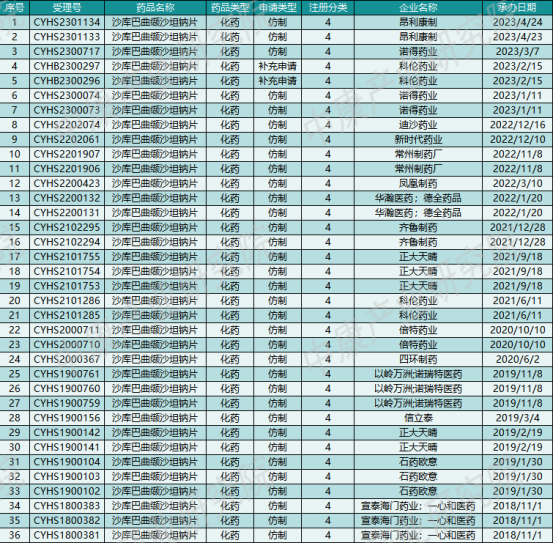

As of the publication date, the CDE has accepted 36 domestic applications (by specification) for sacubitril/valsartan, involving 19 companies. Additionally, about ten companies, including Anglikang Pharmaceutical, Nuode Pharmaceutical, New Times Pharmaceutical, and Phoenix Pharmaceutical, have completed bioequivalence (BE) studies. Another five companies, including Rundu Pharmaceutical, Deyuan Pharmaceutical, Lepu Pharmaceutical, and China Resources Shuanghe Limin Pharmaceutical, are currently conducting clinical trials. It may take some time to see who will ultimately secure the "first generic" approval.

Table 3: Generic Applications for Sacubitril/Valsartan Accepted by CDE

04. Conclusion

With the deepening of population aging and the accelerating pace of modern life, the number of people with hypertension is rising year by year, and the market size is continuously expanding. How to enter this fiercely competitive field of antihypertensive drugs is a strategic question many companies need to consider.

From the author's perspective, approaches for antihypertensive drug development can focus on the following aspects:

Development targeting new drug targets and mechanisms of action, such as dopamine β-hydroxylase (DβH) inhibitors, soluble guanylate cyclase (sGC) stimulators, etc. Another approach involves leveraging sustained/controlled-release formulation technologies to enhance the slow-release profile of drugs, achieving "new uses for old drugs." A third is the development of combination formulations to address combination therapy needs or treat specific patient populations.

Of course, lifestyle intervention remains a highly effective means of preventing and controlling hypertension. In daily life, this includes reducing sodium intake, increasing potassium intake, maintaining a balanced diet, controlling weight, not smoking, limiting alcohol consumption, increasing physical activity, achieving psychological balance, and managing sleep. These measures can effectively prevent and reduce the occurrence of hypertension.

Previous:

Previous: Back to List

Back to List